Blockstar Research Report: Ethereum (Part 1)

Blockstar Research Report: Ethereum (Part 1)

Into the merge; Insight into the state of Ethereum, and the first steps to a potential valuation post-merge

Contents

Ethereum Background

State of the Network

State of DeFi, NFTs, Stablecoins, and Layer 2s

EIP 1559 and The Merge

Post-Merge Projection

Ethereum Background

Overview

Ethereum was introduced to the public in November of 2013 when Vitalik Buterin released the project’s first whitepaper. Vitalik based his concept of a decentralized network on the emergence of Bitcoin, the first digital currency that has no central authority or issuer. Rather, Bitcoin introduced the concept of a decentralized network run by a community of computers. Vitalik, widely considered one of the geniuses of crypto, saw the opportunity to take this blockchain concept, and apply it to all forms of digital ownership through the creation of smart contracts.

Smart Contracts

A smart contract is a program that runs on the Ethereum blockchain and is deployed by the network of nodes (participants on Ethereum). Each smart contract contains a collection of code and data that resides at a specific address on the Ethereum blockchain. When various inputs are created that are deemed to be valid, the network approves and guarantees a certain output.

The easiest way to conceptualize the concept of smart contracts is to think of them as digital vending machines.

The introduction of smart contracts on Ethereum allowed for the development of decentralized applications to be built on top of the Ethereum blockchain. In theory, digital ownership can be applied to almost anything as is evidenced by the creation of NFTs, decentralized autonomous organizations (DAOs), and tokenized real estate.

Ethereum Foundation

Because Ethereum is decentralized, there are no company directors to determine the direction of the project. Instead, Ethereum is developed and advanced by the Ethereum Foundation, a non-profit organization dedicated to supporting Ethereum and related technologies. The Ethereum Foundation consists of all the individuals, developers, companies, and organizations committed to seeing the success of the ecosystem. In essence, the network is run by its users, and the success and efficiency of the network are determined by the growth of its participants.

State of the Network

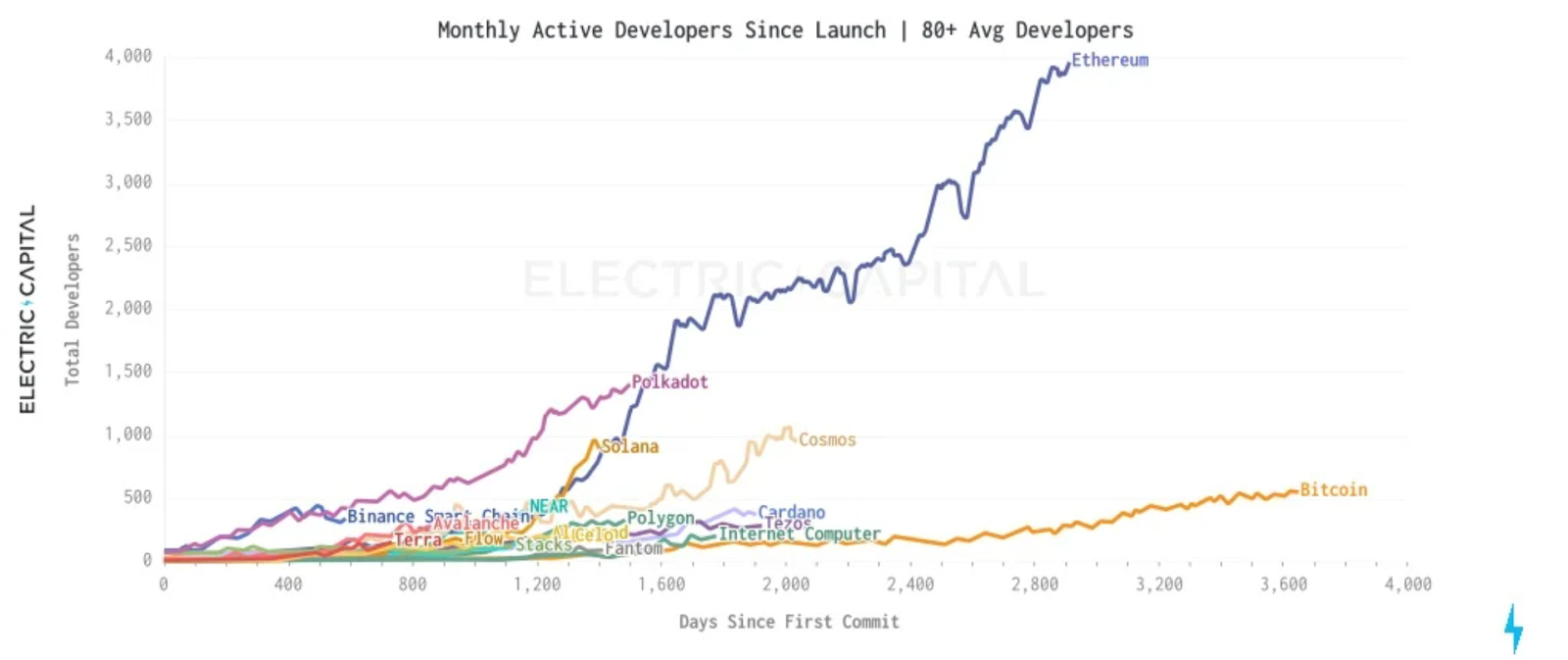

There are a number of publicly available data sets that can be used to measure the performance of the Ethereum ecosystem. The first and most important metric for any layer one is the number of active developers currently working on that network. Without an active community of developers upgrading the network and building protocols for people to use, it is difficult for a network to accrue value. Ethereum’s developer pool is diverse and continuing to expand, standing out among other protocols and creating noticeable value. Out of the estimated 18,000 Web3 developers, 4,000 of them call Ethereum home. Undoubtedly, Ethereum benefitted from a first mover advantage for a blockchain with smart contract functionality, but this is not the sole reason for its ability to attract developer talent. We would argue it is mostly due to a wealth of developer tools, tutorials, learning materials, testnets, and in general the overall ease of use compared to other networks.

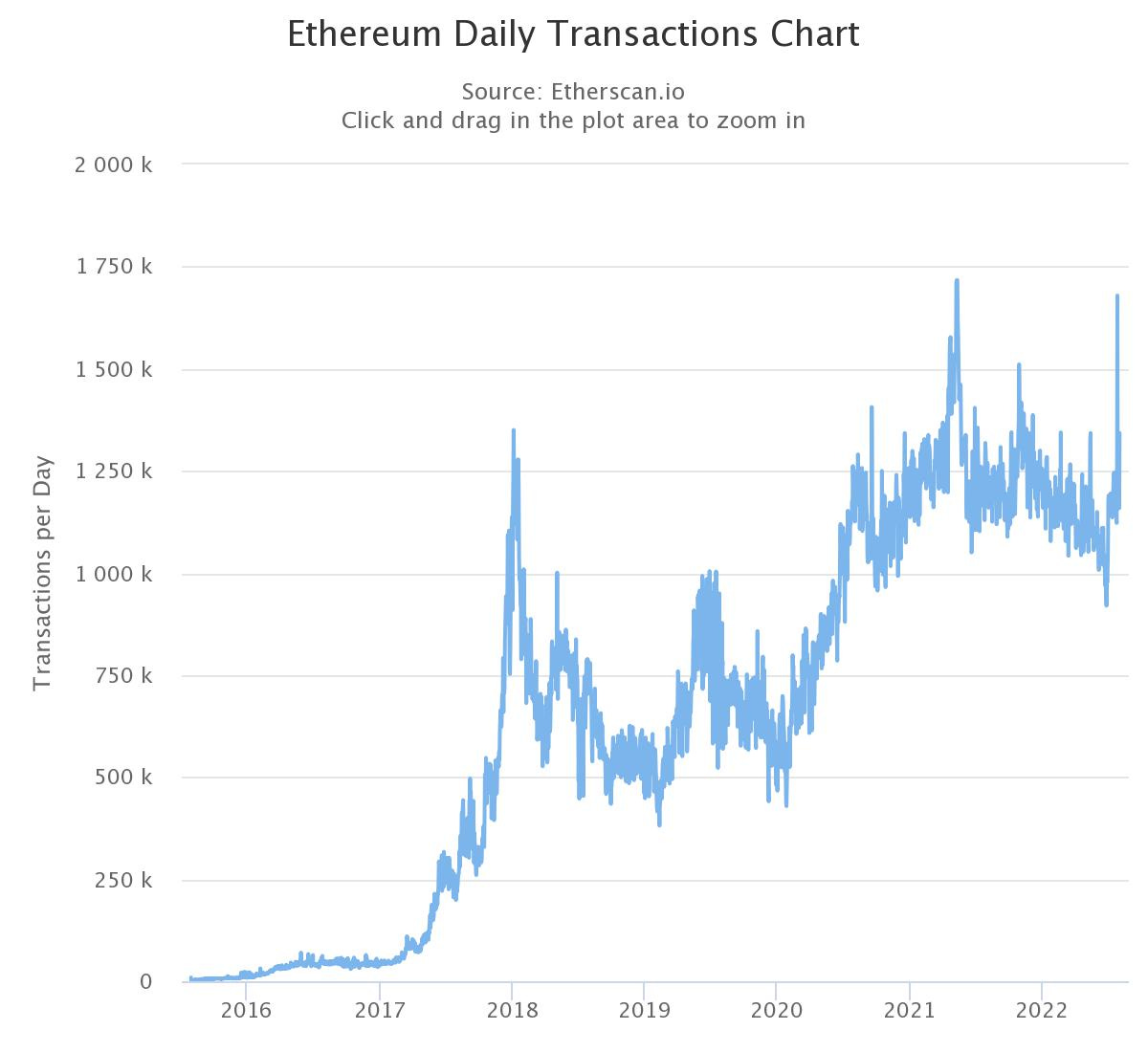

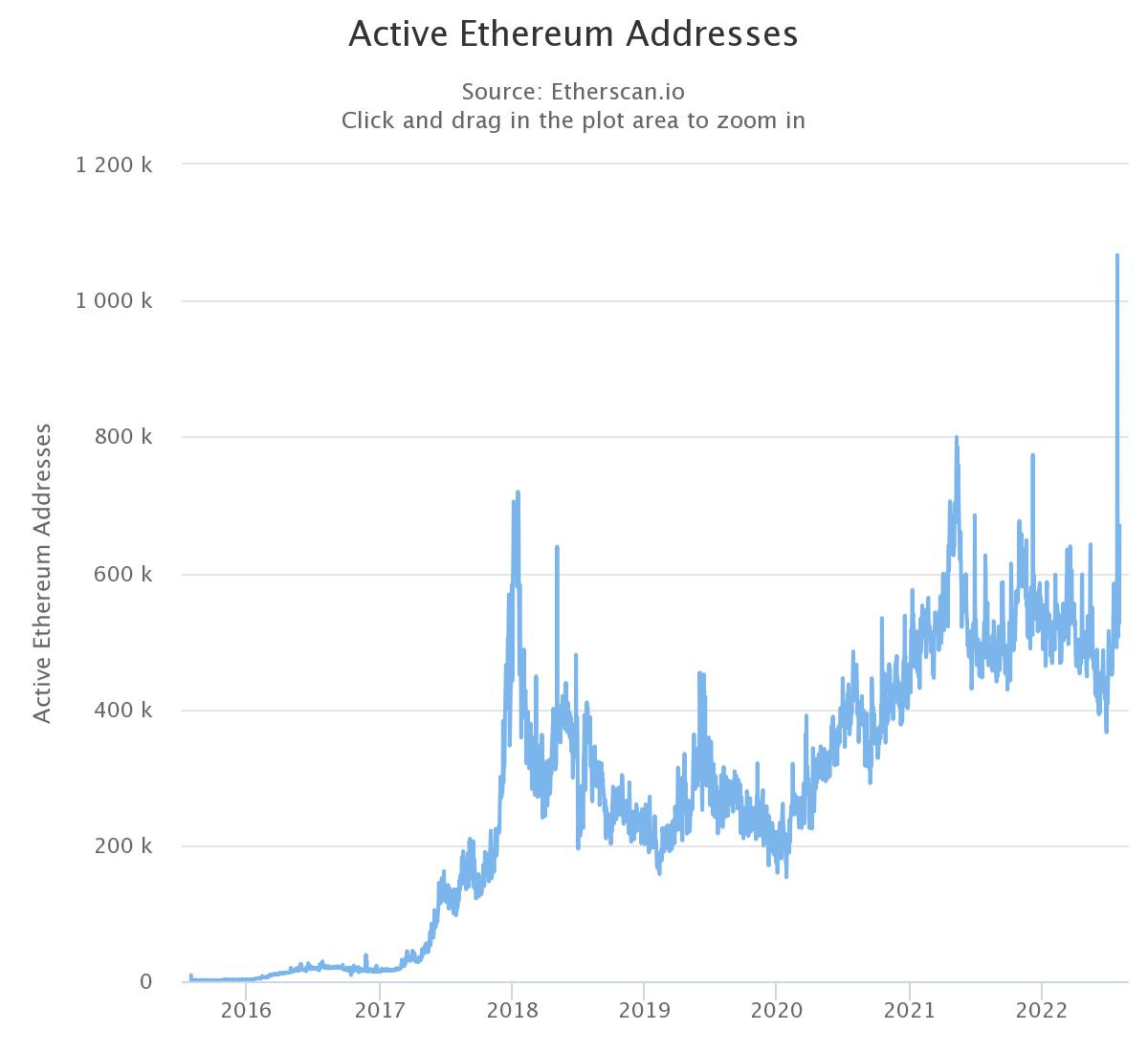

With a strong base of developers, the next metrics to look at are active Ethereum addresses and Ethereum daily transactions. These measures help us identify how active users are on the network. From both of these charts, we can see that over the life of Ethereum there has been a general upward trend. As of now, both active addresses and daily transactions are significantly higher than the prior 2018 bear market, and not far off from 2021’s bull market. Essentially, people may have walked away from crypto following the recent downturn, but there is still a large community active and transacting on the network. This makes sense when you compare this market cycle with the previous. Most of the products built then were simply vaporware. Most of the activity of crypto users was done on centralized exchanges trading one ICO coin for another. Things really began to change when DeFi protocols, NFTs, and stablecoins were introduced.

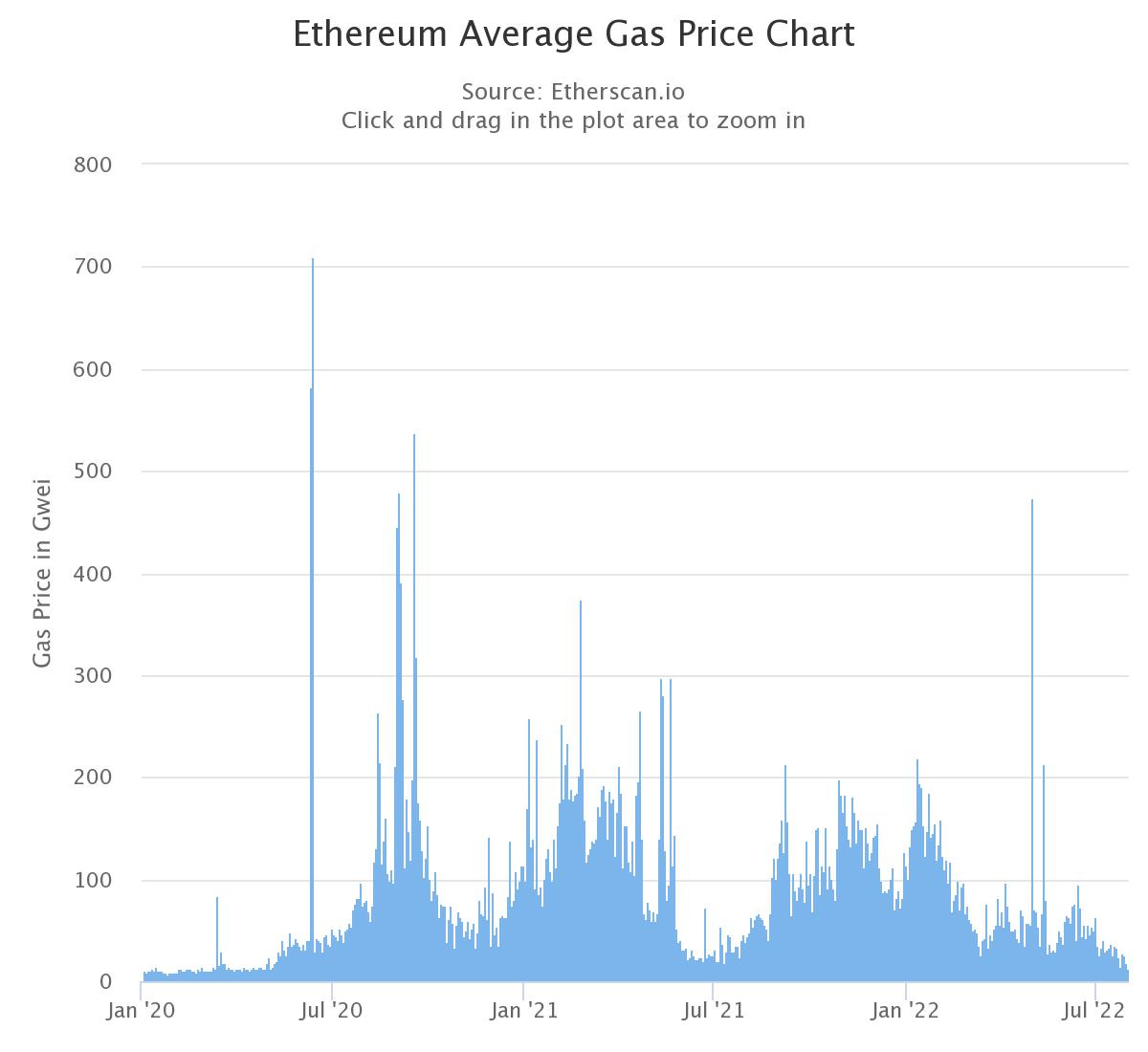

Although the two charts above paint a positive picture for Ethereum, the one that matters most is not as rosy. As mentioned, the introduction of DeFi and NFTs was fundamental in driving on-chain transactions. Once the market started to turn, most of the activity and fees paid to the Ethereum network subsided. Looking at the chart below we can visualize the decline in average gas price for the network. Currently, the seven-day average fees paid to Ethereum clock in at $3.3M while at the peak in November 2021 the seven-day average was $64.2M. This is a 94% decrease in fees paid to the Ethereum network.

State of DeFi

One of the most exciting things to have the pleasure of watching develop has been decentralized finance (DeFi). DeFi is the first open and transparent financial system that is built on blockchain technology offering true control and visibility over your money. It is a financial ecosystem gives anyone around the world the ability to lend, borrow, long/short, earn interest, and more on their crypto assets without the need for human intervention. This automation and transparency were critical during this recent downturn as crypto users were able to monitor the health and solvency of DeFi protocols like Aave or Compound. Contrary to what the media has reported, it was actually the centralized entities like 3AC or Celsius who caused issues because their balance sheets were not verifiable on-chain. But still, when these centralized entities became insolvent they had no choice but to pay back their loans on DeFi protocols first, as the smart contracts are simply computer programs that act based on a predefined set of rules; there is no room for negotiation with a smart contract. We believe the performance of DeFi protocols in this recent downfall greatly legitimizes their ability to act as a transparent and effective financial system.

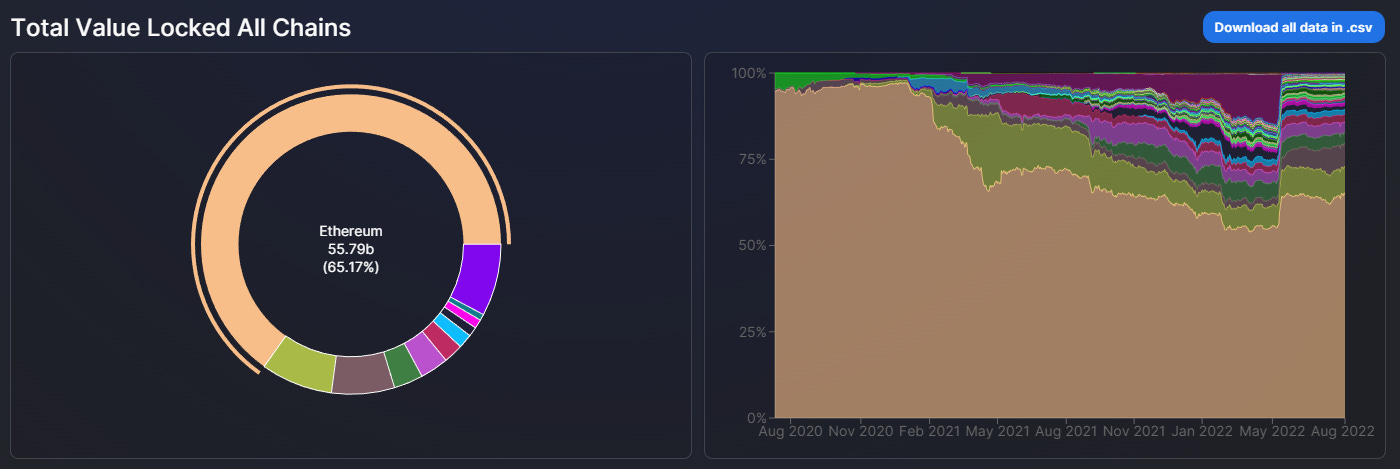

Although DeFi protocols are accessible on any blockchain, most of this financial activity has occurred on the Ethereum network due to its superior security and liquidity. The largest and most trusted protocols like Uniswap, Aave, MakerDAO, and Curve are all Ethereum native, and only later offered their services on other blockchains. Of the $86 billion currently deployed in DeFi protocols, over $55 billion of this is on Ethereum.

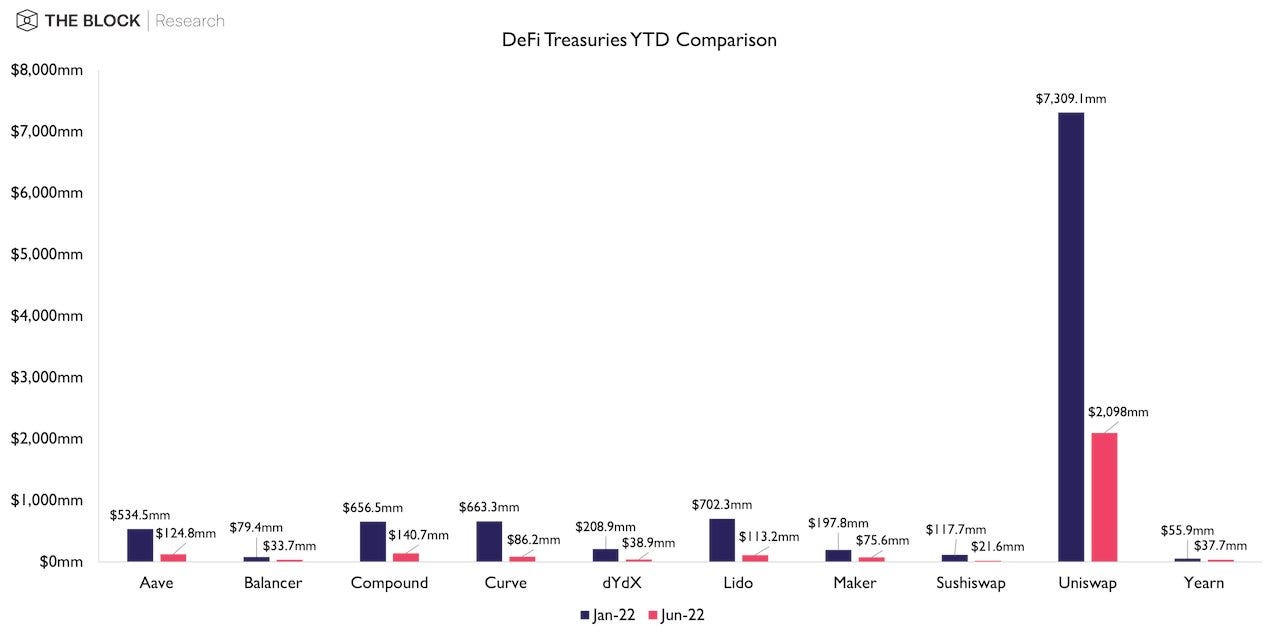

As these DeFi protocols have gained in popularity, they have also benefited from lucrative fee models. As you’ll see below, many of the most popular DeFi protocols have amassed treasuries in the hundreds of millions of dollars, with Uniswap sitting on a treasury of over $2 billion even with deflated prices.

We can make two key observations from this information. The first is these protocols were able to effectively create a blockchain product that drove user and revenue growth. Even now, Curve Finance offers a 5.77% APY (30d average) for CRV stakers paid out in a stablecoin with revenues generated from trading fees. The second, is the most trusted and popular DeFi protocols are well capitalized to continue innovating through this bear market, and for years to come. We have truly only scratched the surface of what DeFi can do, and it will be even more exciting to watch as DeFi continues to evolve.

State of NFTs

Similar to DeFi, NFTs are still in their early stages, although even the earliest Bitcoin developers like Hal Finney saw a future for digital trading cards with provable authenticity and ownership. Non-fungible tokens, or NFTs, have created a means to digitally represent ownership of unique items on the blockchain. Most commonly, NFTs have been used to represent things like art or collectibles, but the technology can really support proof of ownership for any asset. What NFTs have been able to do so well is build communities around the tech and projects. A clear example of this is the Bored Ape Yacht Club’s Otherside mint. Over $150M in Ether was forever destroyed as a result of thousands of users trying to mint these NFTs at the same time, congesting the Ethereum network.

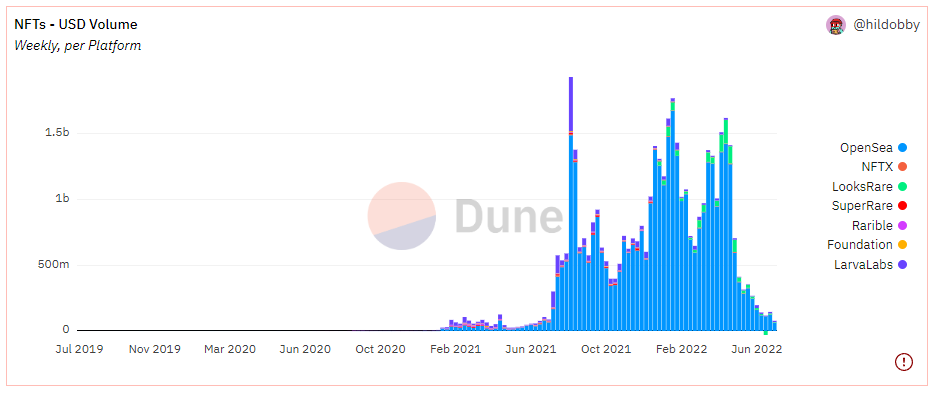

There is no denying that NFTs have performed as the most speculative asset in crypto, akin to the shitcoins of cycles past. The vast majority of NFT projects targeted this hype for a quick buck and left their investors holding the bag. At the peak, NFT trading volumes were over $200m a day with peaks near $600m, but today NFT trading volumes are stagnant, trending between $10-20m per day. The wind has been removed from the NFT sails, but they still provide value to the general ecosystem in a number of ways. From a fee perspective, Opensea is still consistently in the top five for contracts that consume the most gas daily.

Fees aside, NFTs are unique because they appealed to the general population. A first-time crypto user is most likely going to look at a DeFi protocol whitepaper and get lost in the jargon - likely deterring them from participating. On the other hand, a first-time crypto user can look through five different NFT collections and choose which one is personally most appealing and purchase it without much technical know-how. For this reason, we consider NFTs a trojan horse to bring more users into the crypto ecosystem as more use cases are developed. NFTs have the unique ability to mesh into the video game world through metaverse and GameFi integration. We saw glimpses of this with Axie Infinity, DeFi Kingdoms, and NFT Worlds. If a blockchain game is able to gain significant traction on say, an Ethereum layer 2, it could provide a means to onboard millions of users into crypto while generating significant value to the Ethereum network.

State of Stablecoins

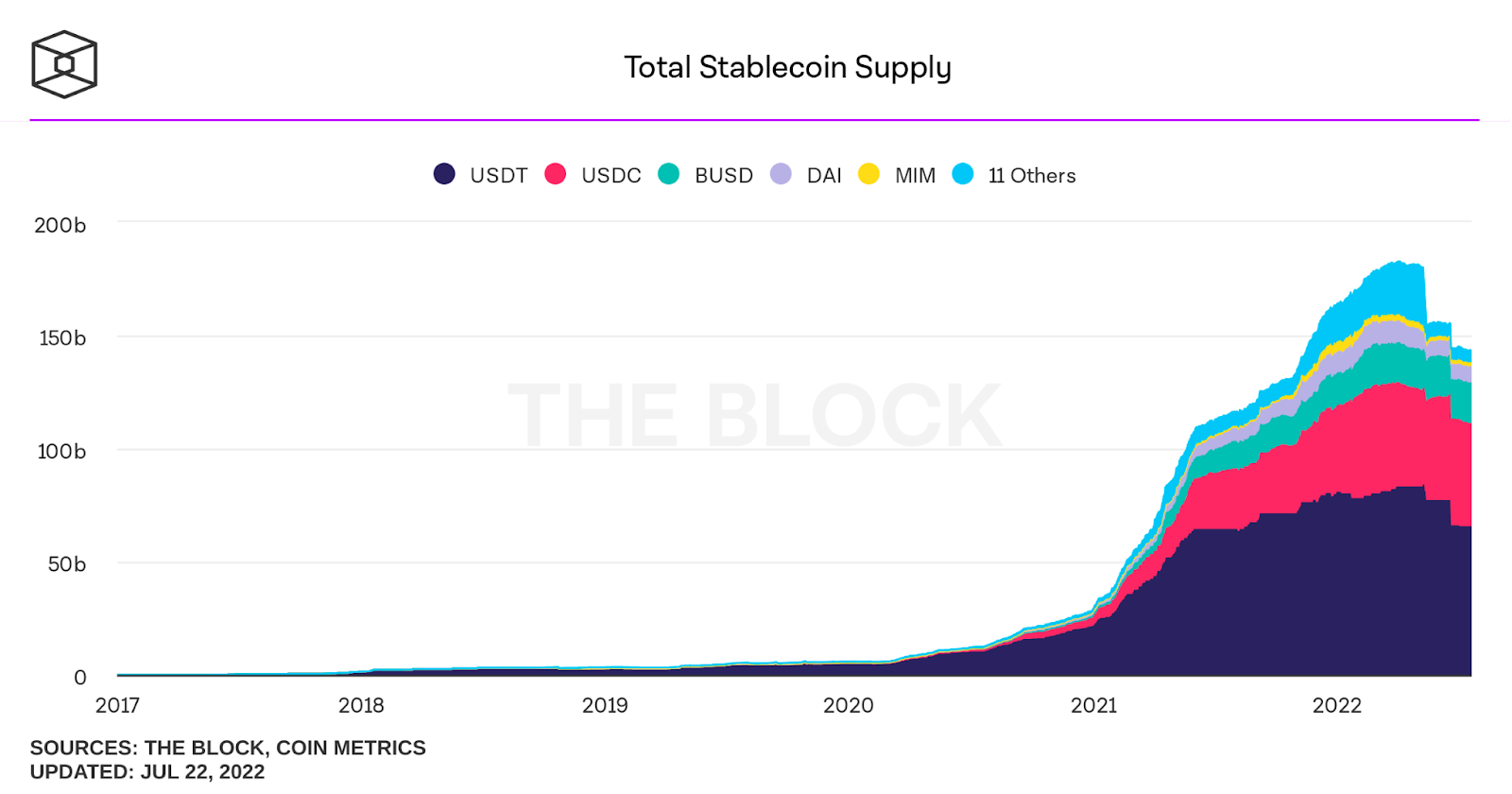

Stablecoins are a key driver in Ethereum valuation. The relationship between stablecoins and Ethereum is mutually beneficial. Stablecoins allow for transactions across borders to global markets. They are fully auditable, creating consistent value for Ethereum, and most importantly, they are interoperable with the rest of Ethereum and its ecosystem. Today, 60% of all stablecoins are issued on Ethereum and are worth about $92 billion.

The velocity of money has greatly improved in crypto since stablecoins were introduced on-chain, bringing both economic growth to Ethereum along with less volatility and more maturity.

However, more noticeable is the bridge that stablecoins have created between traditional finance and crypto markets. Financial products like borrowing, lending, and derivatives need a stable and reliable base value. The Ethereum ecosystem is also giving individuals the option to avoid inflation in less financially developed countries, all through stablecoins and similar financial products. There is no coincidence that governments have taken notice of Central Bank Digital Currencies (CBDCs) and their network effects.

Some key metrics to understand the value being transferred on Ethereum through stablecoins are total stablecoin supply and the key stablecoins on Ethereum.

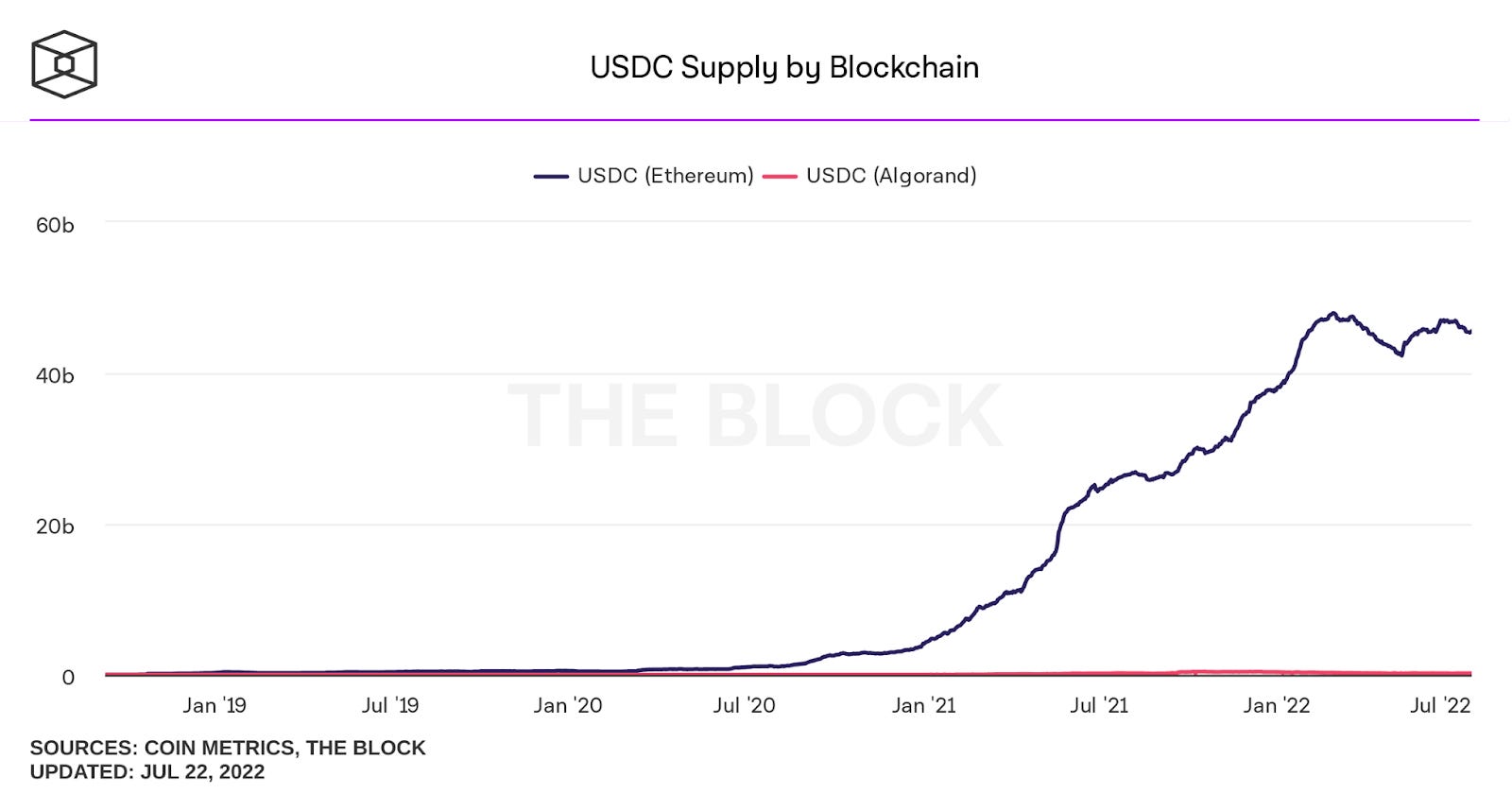

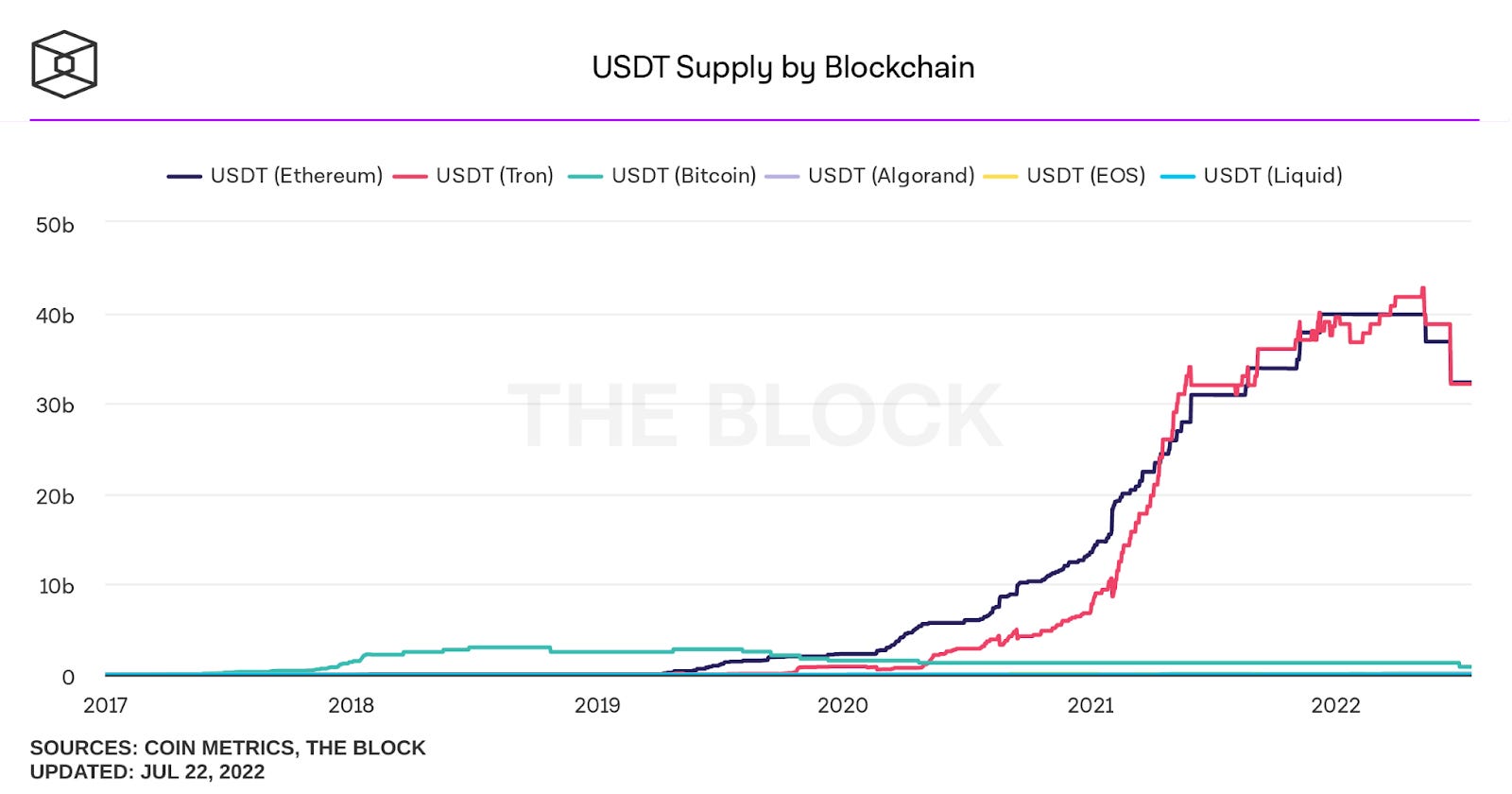

The total stablecoin supply sits at around $150 billion with the largest stablecoins being USDT, USDC, and BUSD. Of this supply, the total Ethereum stablecoin market cap is $92 billion. The two largest stablecoins on Ethereum are USDC and USDT. Both USDC and USDT also contribute significantly to Ethereum fee revenue as they are the most highly transacted coins on the network.

USDC supply on Ethereum is around $45 billion while USDT supply on Ethereum is sitting at just over $32 billion.

Looking at the relationship between Ethereum and stablecoins there are clear parallels we can draw with banks, the transfer of money, and the SWIFT network. Behind international money and security transfers is the Society for Worldwide Interbank Financial Telecommunications (SWIFT) system. SWIFT is a vast messaging network that banks and other financial institutions use to quickly, accurately, and securely send and receive information, such as money transfer instructions. This is why the relationship is so important and fundamental when understanding Ethereum’s valuation. Ethereum is in parts acting as the SWIFT network for the decentralized world. We are able to take part, with ownership, in this network. As these charts would suggest, stablecoins on Ethereum are only growing and will continue to grow. This brings immense liquidity to the network, aiding to the expansion of Ethereum’s economy.

State of Layer 2’s

The growth of layer 2 networks is yet another cog in the machine that drives value to Ethereum. The common complaints with Ethereum are that the network is slow and expensive. During the previous bull market, some users were effectively priced out of Ethereum as a single trade on a decentralized exchange like Uniswap could cost upwards of $100 in gas fees. This is what led to the introduction of so many new layer one networks that were designed to be Ethereum killers. Although we cannot say for certain that another layer one network won’t surpass Ethereum, we find this very hard to believe with the introduction of layer 2s.

A “Layer 2” is the name given to networks that process transactions off of a layer 1 but inherent its security. Essentially, a layer 2 batches transactions together and then anchors them to a layer 1 significantly reducing fees and wait times. By regularly anchoring these transactions on the Ethereum mainnet, it allows the layer 2 to inherit the security, and immutability of the Ethereum network.

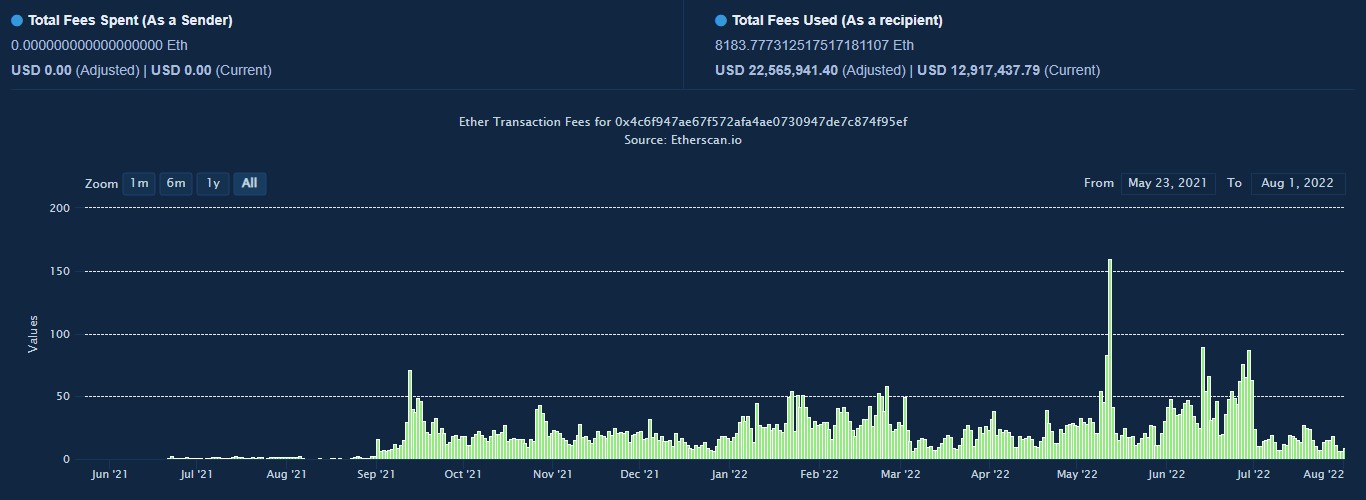

What some investors get wrong is that they see these layer 2 networks as a threat to Ethereum, rather than a benefit. Sure these layer 2 networks will take some activity off of the mainnet, but they still have to pay to anchor these transactions.

Using Arbitrum, a popular layer 2 as an example, we can see in the graphic above how much a single sequencer is paying to Ethereum for security. If Arbitrum and other layer 2s continue to grow and offer an opportunity for cheap, fast, and secure transactions, the benefit to Ethereum mainnet will only grow. If you believe in the growth of the general ecosystem it is clear layer 2 networks are a net positive for Ethereum. Today there is already a handful of layer 2 networks like Arbitrum, Optimism, Metis, Boba, and Loopring. We expect these networks will continue to grow, and provide significant value to Ethereum in the long term.

The insights proposed regarding DeFi, NFTs, stablecoins, and layer 2s illustrate the enormous strides the ecosystem has made in the past few years. While the progress is promising, we are a long ways off from where Ethereum needs to be to become a viable open financial system for the masses. Given the insight of where the demand for blockspace is generated, we can begin to shape a valuation around Ether. However, two fundamental changes to Ethereum, EIP-1559 and the Merge, will have drastic impacts on any potential projections and therefore must be taken into consideration.

Fundamental Changes to Ethereum

EIP-1559

Ethereum Improvement Proposal 1559 was first suggested in April of 2019 and implemented on August 4th, 2021. Prior to EIP-1559, Ethereum used a simple auction system to price transaction fees. Users would have to essentially outbid other users by setting higher gas fees to get their transactions processed by miners faster. This resulted in highly unpredictable and expensive transactions for the average user. This simple auction system also resulted in unspecified wait times as it was unknown whether other users would outbid you. To remedy this inefficiency, EIP-1559 replaced the simple auction system with a base fee model where the fee fluctuates dynamically based on network activity. In this model, the base fee is adjusted by the protocol based on how much demand there is to use the network at that time. This results in a more predictable fee since the fee is slightly changed based on the gas usage per block. In addition to this base fee, there is also the priority fee. This fee allows users to ensure their transaction is included in a specific block. For example, if the base fee is currently 20 gwei, a user may decide to add a priority fee of 3 gwei to ensure the transaction is completed as soon as possible. Between the base fee and priority fee, users are given more predictability and customization while transacting on the Ethereum network.

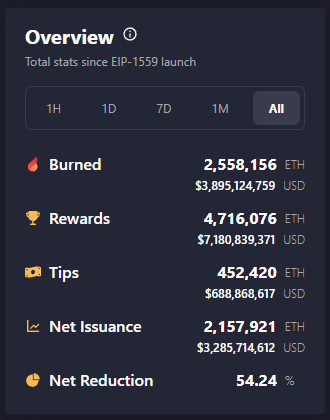

Once it is understood how EIP-1559 works, the impact it has had becomes clear. The most important thing to note is that prior to this change the entire gas fee from a transaction would go to the miners. Post EIP-1559 only the priority fee is given to the miners, while the base fee is burned, removing it from supply forever. This has had a dramatic impact on the inflation in the network. Since EIP-1559’s launch, there has been a 54% net reduction in ETH emissions with over 2.5M Ether permanently burned. This impact has been significant pre-merge and has even stronger implications post-merge.

The Merge

The most significant change to happen to Ethereum is the Merge. This will be the transition from the energy intensive Proof of Work consensus model to a Proof of Stake consensus model. Miners will no longer secure the network, in favor of using staked ETH as validators to secure the network and earn a yield for doing so. These Proof of Stake validators will assume the role of the miners before them taking on the responsibility for processing the validity of all transactions and proposing blocks. This upgrade to the network has been years in the making and the cause of debate not only within the Ethereum community but the general crypto community as well. With that said, there are a couple of main takeaways for this change.

For ESG investors, once the switch to Proof of Stake happens the energy usage of the network is expected to drop by 99.5%. Currently with Proof of Work consensus, miners are using their computer power to solve puzzles whereas the energy used to solve these puzzles act as proof that real world value was invested for the right to add a block to the Ethereum blockchain. Now that the network has grown sufficiently in size and value, the need for energy to prove value was invested into the network will be swapped for the value from ETH staked as a validator. There is no longer a need to secure the network with significant amounts of energy.

As a result of the network no longer requiring vast amounts of energy to secure transactions, there is no longer a need to pay a large subsidy for the costs of that energy either. In the current PoW model, there is currently ~13,000 ETH distributed each day as mining rewards. Post merge, this will be reduced to ~1,600 ETH distributed to validators each day. If you consider the impact of EIP-1559, at an average gas price of at least 16 gwei per day the daily inflation would be negated. If there was an average gas price of anything higher than 16 gwei, Ethereum would become a deflationary asset. Beyond this, we will also see a significant reduction in the sell pressure put on Ether price by Ethereum miners. Given the cost intensive nature of mining cryptocurrencies, miners are often left with no choice but to sell what is earned each day to run a profit. With roughly 13,000 Ether in mining rewards each day that is $20M worth of possible sell pressure, every single day.

As you can see, the Merge has serious implications for the future value of the Ethereum network. All we can do now as investors is patiently await the September 19th estimated merge date, and put together potential valuations for the future of internet money, Ether.

Post-Merge Valuation Projections

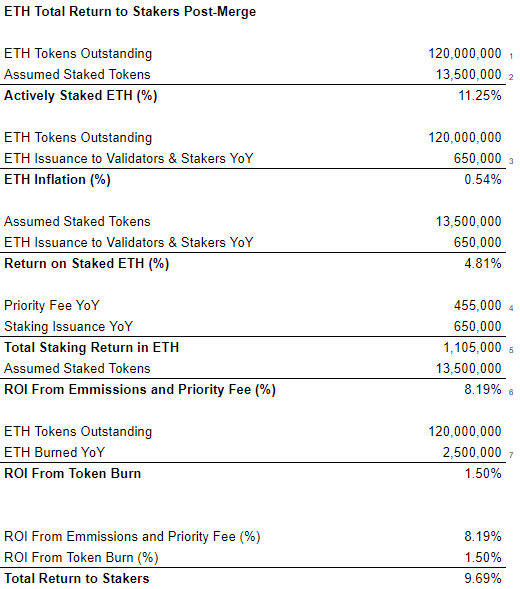

Given the understanding of where the demand for blockspace comes from and the changes implemented by EIP-1559 and the Merge, we can now begin to create a projection for post-merge Ethereum. Keep in mind, this is still highly speculative and is used as a first step in producing an economic valuation model for Ether. For the purposes of this projection, since EIP-1559 was enacted almost a year ago to this day, we have decided to use transaction data from the last year. Based on this data, 2,500,000 Ether have been burned and 455,000 Ether were included in transactions as a priority fee. Given a current staked supply of 13,200,000 Ether, we have estimated this figure to rise to 13,500,000 during the time of the Merge which is in line with the growth of deposits over the previous month. Based on this amount of Ether staked, we can estimate the protocol emissions to be roughly 650,000 Ether per year according to the suggested staking rewards from the Ethereum Foundation.

Below, you can see an example of some of the metrics and ratios we would use as inputs for our model.

Given the inputs above, we can estimate the ROI from protocol emissions and transaction fees to come out to a roughly 8.19% ROI. If you consider the net income from burned Ether, the total return to stakers would equate to roughly 9.69%.

Because the nature of the protocol is changing post-Merge, we do not have the appropriate data to confidently opine on the value of ether as it stands today. However, we believe that the post-Merge economic data will allow us to build an appropriate model with the right data points. The data that we will be collecting as our main drivers in our model include:

Total ETH Circulating Supply

ETH Staked Supply

ETH Emissions

ETH Burned

ETH Paid as a Priority Fee

With these inputs, we are confident we will be able to adequately project the circulating supply, which is the first step toward putting a dollar value on the token. In addition, we will consider the ETH emissions (the amount of ETH returned for staking) to be able to quantify the return and therefore the value of 1 Ether. As these progressions occur, and the data begins to form, we will be able to provide updated models for valuing ether. Until then, we consider this a solid foundation for valuation consideration into a once purely speculative asset class.