DeFi Yields

As you are chasing yields in decentralized finance, it is crucial to know exactly where this yield is coming from and what this yield is paid out in. A yield paid out in a native token is not nearly as attractive as a yield paid out in a stablecoin or ETH. At the height of the crypto market, most people were not asking these questions and this is how we became accustomed to yield farms offering 100+% APY in some quickly generated, useless token. Obviously, this is not sustainable and all of these farms have died out or are on their last breath. Those protocols that have figured out a way to offer a sustainable yield in a non-native token are those that certainly make the bag holding easier, but may also prove to be viable long-term investments. This week we will look at a number of DeFi protocols that offer yields that have proven to be sustainable as well as how these yields are possible.

CRV - Automated Market Maker

The first protocol on the chopping block is Curve Finance, an automated market maker that specializes in like-assets. What this means is Curve focuses on liquidity pools that in theory should trade at the same price, like stablecoins (USDT, USDC, DAI) or wrapped coins like (wBTC, renBTC, sBTC). When users want to swap from one asset to another they can utilize the liquidity pools on Curve. To do so, users pay a fee that can range between 0.01% and 0.4%. From these fees, 50% goes to users who provide liquidity to these trading pools and the remaining 50% goes to users who stake their CRV with the trading fees paid in 3CRV, a basket of stablecoins. At face value, this may not seem like a lot but Curve has grown to become one of the most trusted and highly liquid AMMs in DeFi and as a result, they have some of the highest trading volumes in DeFi. Below you can view trading fees accumulated and dispersed to CRV stakers this year.

Currently, the 30-day staking APY comes out to 14.83%, and a P/E of 6.74 for staked CRV. A very attractive investment for most DeFi investors. As Curve continues to dominate the AMM scene and move into pools that offer unlike assets, it will be interesting to see if other AMMs will be able to compete at a high level. With such a high demand for CRV given the yields you can earn, Curve Finance has created a very strong ecosystem for users and protocols to trade.

GMX - Decentralized Perpetual Exchange

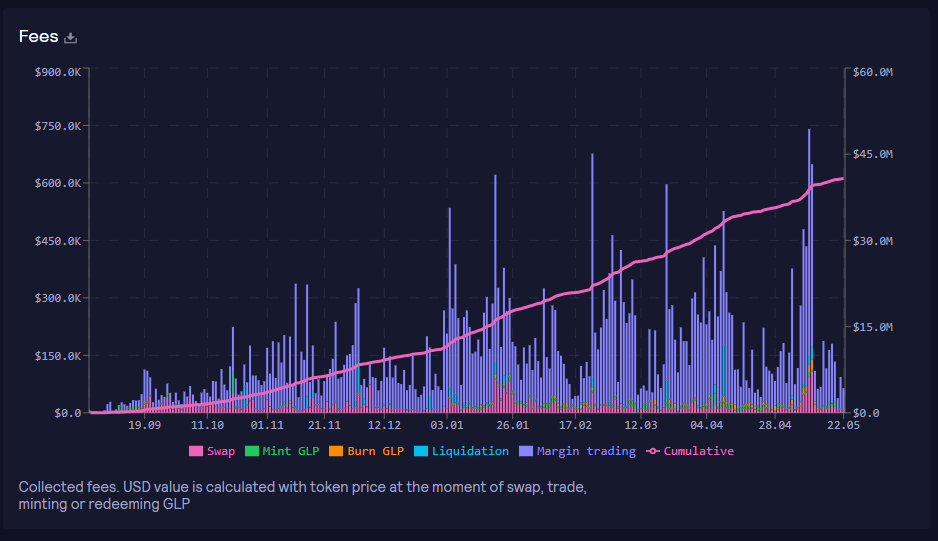

The next protocol is GMX, a decentralized perpetual exchange that is currently live on Arbitrum (an Ethereum Layer 2) and Avalanche. GMX allows users to trade with up to 30x leverage on popular coins like ETH, BTC, LINK, and UNI. What is unique about GMX is that they are able to offer users leverage in a completely decentralized way through utilizing their liquidity pool token GLP, which in a nutshell is an index of assets used for swaps and leverage trading. All a user needs to begin trading is a wallet like MetaMask; there is no need for a username or password. To date, GMX has done over $30 billion in volume which at the time of writing provides GMX stakers with an estimated APY north of 30%. Over the last few months, active traders on the site have begun to explode to over 20,000 total users.

Well, how is it possible for GMX stakers to earn such a high yield? For every user that opens a trade a 0.1% fee is incurred based on position size, and on closing the trade they must again pay a 0.1% fee based on position size. Of these fees, 30% go to GMX stakers paid in ETH on Arbitrum and AVAX on Avalanche. We sure do love yields not paid in a native token! For investors that may not be keen to try their hand at leverage trading, GMX offers them a unique ability to act as the house. As the bear market rages on, GMX offers traders a smooth trading experience and GMX investors an impressive yield. Although the competition in the decentralized leverage trading scene is fierce, GMX’s unique tokenomics have made it one of the favorites for DeFi traders and investors alike.

LOOKS - NFT Marketplace

As NFTs continue to prove they are here to stay, there has been a flurry of new marketplaces popping up promising to be the Opensea killer. With a 2.5% fee on every NFT sale, Opensea has done quite well for itself. Recently, Opensea has also opened up markets for Polygon and Solana NFTs as well.

To give Opensea a run for their money, Looksrare developed an NFT marketplace that charges a 2.0% fee on sales and instead of going to a centralized entity, 100% of this fee is dispersed among LOOKS stakers. At the time of writing, the current APR paid out in wETH is 22.52% (plus an additional 21.43% in LOOKS emissions, but we don’t talk about native token yields here).

Although Looksrare arguably offers a more lucrative experience for users by offering lower fees, trading rewards and even paying users in LOOKS to list on the marketplace, there is still an uphill battle to dethrone Opensea. The first-mover advantage is certainly amplified in crypto and is no different in terms of NFT marketplaces. Either way, if Looksrare can maintain the market share it already has, users can expect to continue receiving a strong APR on their staked LOOKS.

FXS - Fraction Algorithmic Stablecoin

The final protocol we will look at today is Frax Finance and their governance and fee accrual token FXS. With UST and LUNA taking the front stage for the last couple weeks, users are definitely weary about other algorithmic stablecoins at this point. Although the design is very different between the two, we are not here to discuss that today but rather what yield can FXS stakers earn and how is this yield possible. Of the protocols mentioned today Frax Finance is definitely the most intricate in terms of how the yield is created.

At any given moment there is a pre-defined collateral level determined by the protocol. As it currently stands the collateralization ratio is set to 89.25%. What this means is right now, FRAX is 89.25% collateralized by on-chain fully collateralized stablecoins. In order to create FRAX a user must put up 89.25% of collateral in one of the protocol approved stablecoins and the remainder is paid in FXS, which is then burned from circulation. On the other hand, if a user wants to redeem their FRAX, they would receive 89.25% of it in a protocol-approved stablecoin and the remainder in FXS. Depending on the price of FRAX each hour, this collateralization ratio can lower if the price is above $1.00 or rise if the price is below $1.00 by 0.25%.

With the understanding of how the FRAX peg is maintained, we can discuss AMOs or Algorithmic Market Operations. These are smart contracts that are designed to carry out algorithmic market operations without affecting the fractional-algorithmic stability of the FRAX token. This means that AMO controllers can perform open market operations algorithmically (as in the name), but they cannot arbitrarily mint FRAX out of thin air and break the peg. Examples of AMOs in action are putting idle USDC to work in DeFi protocols, rebalancing liquidity pools on Curve or Uniswap, or lending FRAX on money markets like Aave.

As of October 2021, a governance vote has directed 100% of the profits from these AMOs to go to FXS holders, which at the time of writing equates to an APR of 9.94%. Although this APR is not paid in a stablecoin or an asset like ETH, I believe we can still consider it to be a viable DeFi investment due to the proven stability of the FRAX peg over the lifetime of Frax.

Even during the tumultuous events for stable coins following the UST collapse, we have continued to see FRAX maintain its peg. In the scary world of algorithmic stablecoins, Frax Finance has undoubtedly created a robust fractionally collateralized stablecoin that is able to adapt to market demands.

This newsletter aims to shed some light on how different DeFi yields are possible. Most often yields are a result of trading fees on exchanges or marketplaces, but can also come from complex algorithms seen with Frax. In the early days of DeFi, most of the yield users earned was from heavy token emissions which were not sustainable in the long term. These most notably offered APYs north of 100% which was able to attract mercenary liquidity leaving most retail traders in the dust. As DeFi continues to develop it will be interesting to see how the mentioned yields change, and what new players come to the table. Keep in mind, that the tokenomics for these projects should be seriously considered before making any investment because what good is a 20% yield when your principal is down 60%. And finally, as a great crypto twitter influencer once said, if you cannot tell where the yield is coming from YOU are the yield.