Stablecoins

Stablecoins

A basic understanding of USDT, USDC, DAI, MIM and BEAN

“CrYpToCuRrEnCiEs aRe ToO vOlAtIlE tO bE uSeD aS a CuRrEnCy!” I’m sure you’ve heard someone use this argument against cryptos before. What they fail to realize is that there is a stablecoin market of over $180 billion dollars today. Although they aren’t all made the same, it is clear that stablecoins are being used by many and continue to grow. With rumblings of a Central Bank Digital Currency, let’s take a look at how some crypto native projects are creating stablecoins pegged to the value of $1.00 USD.

USDT

Perhaps the most controversial stablecoin out there, USDT has been a prominent player in the space since its inception in 2014. As stated on their website, Tether claims their stablecoin token is backed 1 USDT : 1 USD, so we can classify them as a collaterally backed stablecoin. This claim means every time you see the Tether printer go brrrr, there should be an equal backing of USD held by Tether. This is not exactly the case, and since facing scrutiny about their backing Tether began to release attestations in February 2021. Below, you will see their backing according to their website.

For now, let’s accept that what Tether is saying is true and that they do in fact hold these reserves. These reserves would amount to $81 billion which places USDT right behind ETH and BTC in terms of market cap. There is obviously significant liquidity for large players to move in and out of USDT and if you look below USDT has been able to maintain its peg without any major hiccups since 2019. This depth of liquidity and the ability to maintain the peg has made USDT a fan favorite for many whales, especially since it is widely accepted by centralized exchanges for those wanting to cash out from crypto.

USDT has also established itself in the DeFi world. For example, USDT is part of Curve Finance’s 3pool which allows users to trade from USDC - USDT - DAI with minimal slippage due to over $3 billion of liquidity in the pool. Overall, the trust in Tether seems to come from them being around so long and providing unparalleled liquidity. On the other hand, there are those who wouldn’t touch Tether with a 10-foot pole due to their questionable team, taking so long to provide attestations, and over 80% of their reserves are held in cash equivalents. We have even seen hedge funds like Fir Tree shorting Tether betting that USDT will collapse within the year. Tether also has the ability to freeze USDT issued by them which rightfully scares away many users.

USDC

If you take Tether and remove the shadiness that comes with them you would have Circle’s stablecoin: USDC. They follow the same fully collateralized model but have maintained transparency since they began in 2018 receiving audits from Grant Thornton LLP confirming their USD reserves. With USDC’s market cap following an up-only route since the beginning of 2021, USDC now sits at the number five spot on the cryptocurrencies by market cap list. As seen with Tether, USDC offers deep liquidity and a wide acceptance with centralized exchanges as well as the DeFi world. Below you can see the chart of their peg stability.

USDC is also a member of the 3pool on Curve Finance and continues to act as one of the more trusted stablecoins in the space. There is no shortage of options to stake your USDC in DeFi protocols, and many coins use USDC as a pairing when listing on a DEX. This has resulted in the astronomical rise in USDC market cap over the last year. USDC become an integral part of the DeFi landscape, but it still has one fatal flaw. As mentioned with Tether, Circle also has the ability to blacklist any address and freeze its assets. In a world where financial freedom is of utmost importance, DeFi degens continue to look for a better stablecoin option.

DAI

We talked about some of the dollar-collateralized stablecoin options with USDC and USDT and understand the issues with them. Now we welcome DAI to the party. DAI was introduced to us by MakerDAO in 2017 with SAI, but it became the DAI we know today in 2019. Unlike its counterparts USDT and USDC, DAI is not backed by reserves held in a bank but rather by other cryptocurrencies. By using Collateralized Debt Positions, users can lock whitelisted assets like ETH, wBTC, UNI, USDC, and generate DAI. Well, you may be asking yourself isn’t it incredibly risky for MakerDAO to give out a loan against volatile cryptocurrencies? Yes, in traditional finance it would be, but with smart contracts the protocol is able to minimize risks and as a result has grown to a supply of over $9.2 billion. A key feature of MakerDAO is that each position must maintain a minimum collateralization ratio of 150%. This is important because if a user doesn’t maintain this ratio, MakerDAO is able to liquidate their funds and subsequently sell these funds via an auction system to other users.

As you can see above, the peg has performed better since the beginning of 2021 due to a strong ecosystem of users. Remember, MakerDAO not only needs people to generate DAI using crypto as collateral but it also needs bidders on the liquidated users’ collateral as well. In the case of a Black Swan event where assets in MakerDAO dramatically crash some speculate whether there is a point of no return for DAI. Ultimately, the peg will not be as tight to $1.00 as USD-backed tokens due to the cryptocurrencies giving DAI stability.

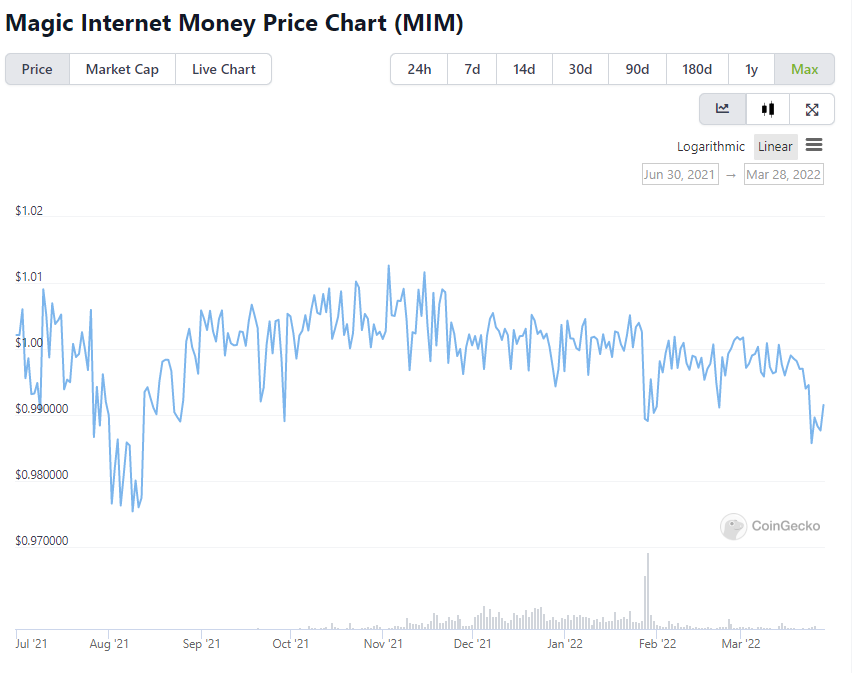

MIM

“ABRACADABRA.MONEY (the protocol) IS A SPELL BOOK THAT ALLOWS USERS TO PRODUCE MAGIC INTERNET MONEY (the stablecoin).” Yup, MIM stands for Magic Internet Money and it has grown to a supply of over $2.7 billion. If you were uneasy hearing DAI is backed by cryptos like ETH or wBTC, you’re surely going to love MIM. Like MakerDAO, crypto is used as collateral for MIM and liquidations keep the protocol solvent. The difference between MIM and DAI is that Abracadabra.Money uses interest-bearing tokens as the collateral to issue MIM against. Up until MIM came about there was a huge supply of tokens sitting idle in popular DeFi protocols like Yearn Finance. Users would take assets like WETH and deposit it into a yield aggregator like Yearn Finance and in turn, the user would receive yvWETH; an interest-bearing receipt of their deposit. There was not anything to do with this interest-bearing token until Abracadabra.Money came around. Now, users are able to take their yvWETH and deposit it in Abracadabra to then mint MIM. This is a key differentiator between MIM and the other stablecoins presented thus far. MIM was not really aiming to be a tightly pegged stablecoin, but it was rather designed to allow users more leverage on their funds in the DeFi ecosystem, which is why we see a loose peg.

The obvious risks of using interest-bearing tokens seem to be presented in the stability of the MIM peg above. As a user, if you are not generating the MIM yourself by posting interest-bearing tokens as collateral it would not be the best decision to use MIM as your stablecoin of choice.

With a questionable development team perhaps Abracadabra.Money’s glory days are behind them. Since a peak in January TVL, fees generated, and the number of new loans are dramatically down. Over the last few weeks, MIM has not even traded at $1.00, making us further question the sustainability of MIM moving forward.

BEAN

Ahhh, time to talk about the Beanstalk. Cryptos that are innovative with audacious goals are always the most fun to research - and that is exactly what Beanstalk is. Starting in September of 2021 with only $100 in liquidity, Beanstalk created a “decentralized credit based stablecoin protocol.” What this means is that their stablecoin BEAN does not require collateral to maintain its peg. Instead, it incentivizes market participants to maintain the peg through the Silo and the Field using things like Weather, Soil, Pods, Seeds, and Stalk. To save your head from spinning all you need to know for now is that when the price of BEAN < $1.00 users (creditors) are incentivized to burn their BEAN in exchange for Pods that harvest at a later date similar to a bond. What this does is reduce the BEAN supply to bring the peg back to $1.00 and allow the creditor to earn a profit when their pods are harvested. On the other side of things, when the price of BEAN > $1.00 new BEANs are minted by the protocol to bring the peg closer to $1.00, and 100% of the newly minted BEAN is given to protocol participants (creditors and governors).

The peg of BEAN has been the most volatile of the stablecoins we have addressed so far. Building an algorithmic stablecoin is no easy feat and every truly algorithmic stablecoin has failed so far. This daunting fact and a supply of just over $45 million make BEAN relatively volatile to other stablecoins. But, since the end of January with the passing of major Beanstalk Improvement Proposals, the peg has more regularly crossed $1.00. With one of the best communities in the space, I have a lot of faith that Beanstalk will continue to grow and become a significant player in the stablecoin space.

Written by: Ryan Celaj