Do Kwon and the Sinking Turd

Do Kwon and the Sinking Turd

Breaking Down Terra USD and the Death Spiral.

Buckle up, I will be taking out the trash that was once Terra USD. For those of you that don’t know, Do Kwon is the mastermind behind the Terra ecosystem… which is currently going through a crypto bank run if you will. Now to save space and head straight for the FUD, I will link our previous work that goes into the mechanics of Stablecoins, Anchor Protocol, and Luna.

Terra USD Peg Maintenance

Terra USD is a stablecoin that is pegged to USD but not backed by USD. Terra offers a redemption promise that allows 1 UST to be redeemed for 1 USD worth of Terra’s native token LUNA.

For example, if UST trades at $0.99, arbitrageurs will,

Buy 1 UST for 0.99 USD —> Redeeming the bought 1 UST for 1 USD worth of LUNA —> Sell the LUNA for 1 USD.

Now let’s be critical in this process and find the risk. Redeeming the bought 1 UST for 1 USD worth of LUNA. Redeeming is a very translucent word. As with any stablecoin, if the redemption process breaks down, so does the peg. Terra’s redemption process is done through burning (redeeming) UST and minting LUNA. Currently, we are seeing selling pressures on both UST and LUNA, which ultimately will put pressure on the redemption process.

Supply Contraction

Selling pressure on UST leads to selling pressure on LUNA. Selling pressure will push UST’s price below $1.00, then arbitrage will set out to correct the peg. This involves minting and selling LUNA for USD. UST is vital for the Terra ecosystem, UST leaving the ecosystem may indicate users have less of an interest in Terra, which can create doubt in LUNA holders, putting selling pressure on LUNA.

Selling pressure on LUNA leads to selling pressure on UST. Luna is THE mechanism that allows for redemptions. If the price of LUNA drops significantly then UST holders will worry about the future availability of these redemptions. Users will sell UST while they still can, creating a crypto bank run.

This cross reliance for both UST and LUNA is called risk. A flood of supply will test the protocol.

De-Pegging Scenario

Is Terra really allowing users to trade 1 USD worth of Luna for 1 UST? Not quite. Terra’s mechanism for exchanging UST to LUNA decreases as more UST is traded per minute. Meaning as UST trades rise per minute, USD value per UST decreases. This mechanism deters the arbitrage process which leads to unbalanced markets. This is what we are currently seeing now, a high period of stress and a large need for peg maintenance.

Picture this scenario. 1B UST holders want to convert to USD as quickly as possible as they see some instability in the market. No one wants to sell at $0.98 or $0.95 per UST. This price will instantly crater towards these prices in hopes for arbitrageurs to buy and burn UST to mint and sell LUNA for USD. We now know this process is only profitable if arbitrageurs can mint LUNA worth more than 0.98 USD per UST. With Terra’s maintenance mechanism described above, arbitrageurs will have a limit on how much UST per minute they can burn to create LUNA in exchange for USD. Meaning for every 1 UST sold for LUNA, the arbitrageurs will only receive 0.98 USD in newly minted LUNA. This process constantly depresses the price of LUNA creating a system where more and more LUNA must be minted for each newly burned 1 UST in order to create the required value of 0.98 USD. This results in a large amount of UST being burned sided with a large amount of LUNA being minted, at an imbalanced amount. This sends LUNA’s price spiraling, bringing no demand, cratering the price. The arbitrage mechanism is broken, cratering the UST peg.

The few that sold left with a 2% drawdown while the rest get flushed.

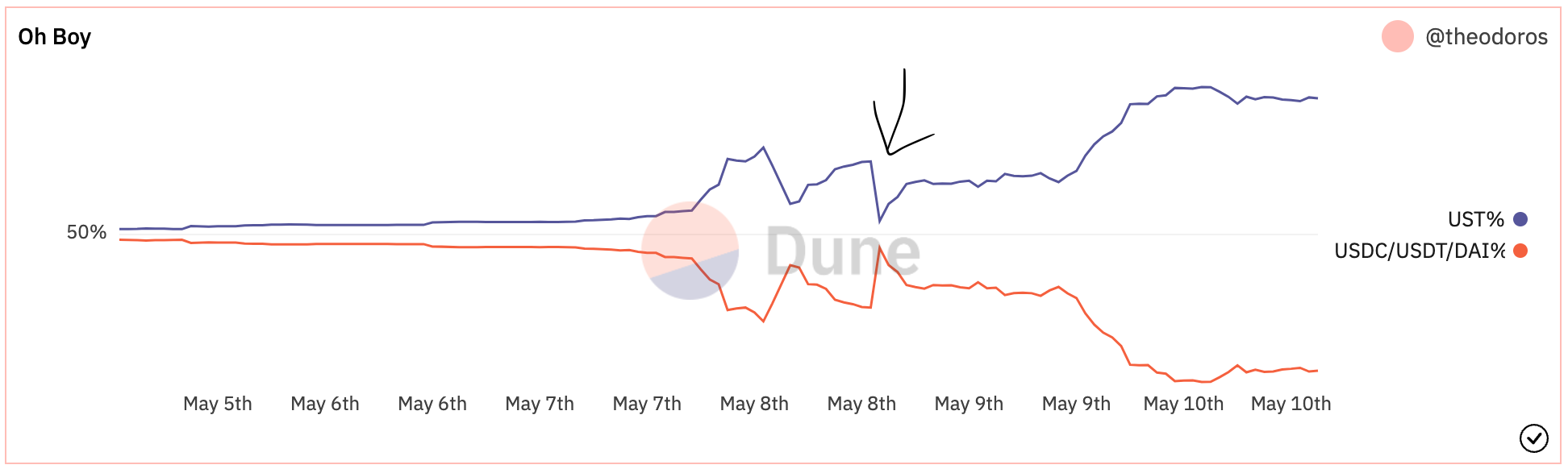

Now let’s connect the dots to what we currently know about the blowup. From what we know there was an imbalance in the UST-3pool. $85 million UST-to-USDC swap occurred to push the pool out of balance. This was followed by selling of $300k to $3M orders on Curve. To put the pool back into balance there was a large offload of ETH (50,000-70,000ETH seen in the picture below) to keep the peg maintained and the pool maintained. Unfortunately, the price never fully recovered after this maneuver. This led to a wave of sell-side liquidity hitting the market and the pool starting to diverge again.

A second address swooped in with a $250M in-load of UST to the pool, essentially holding debt in what was soon to be a very unbalanced pool.

Simultaneously, exchanges were getting hit with waves of sell-side liquidity all while arbitrageurs are trying to keep stability. Now, remember, there is no arbitrage if you don’t eventually sell, it’s just debt. The second address had close to 580 million of unsellable UST and then the price began to tank after 0.98 UST was lost. This brought our scenario described above into full effect.

As time plays out we will see which VCs or Funds run to the rescue with liquidity to hopefully help price stability. I was and am still a fan of the idea of Terra and the ecosystem, but it is clear the mechanisms involved were somewhat flawed and bound to be stress tested. Unfortunately, fortunes were lost and Mike Novogratz’s Luna tattoo is looking really comical.

Written by Theo White